August 26, 2025: The U.S. housing market continues to reflect the combined pressures of affordability, mortgage rates, and shifting buyer demand. Two closely watched measures—the NAHB/Wells Fargo Housing Market Index (HMI) tracking prospective buyer traffic and the Mortgage Bankers Association (MBA) Purchase Index—illustrate the patterns shaping the market from 2020 through 2025.

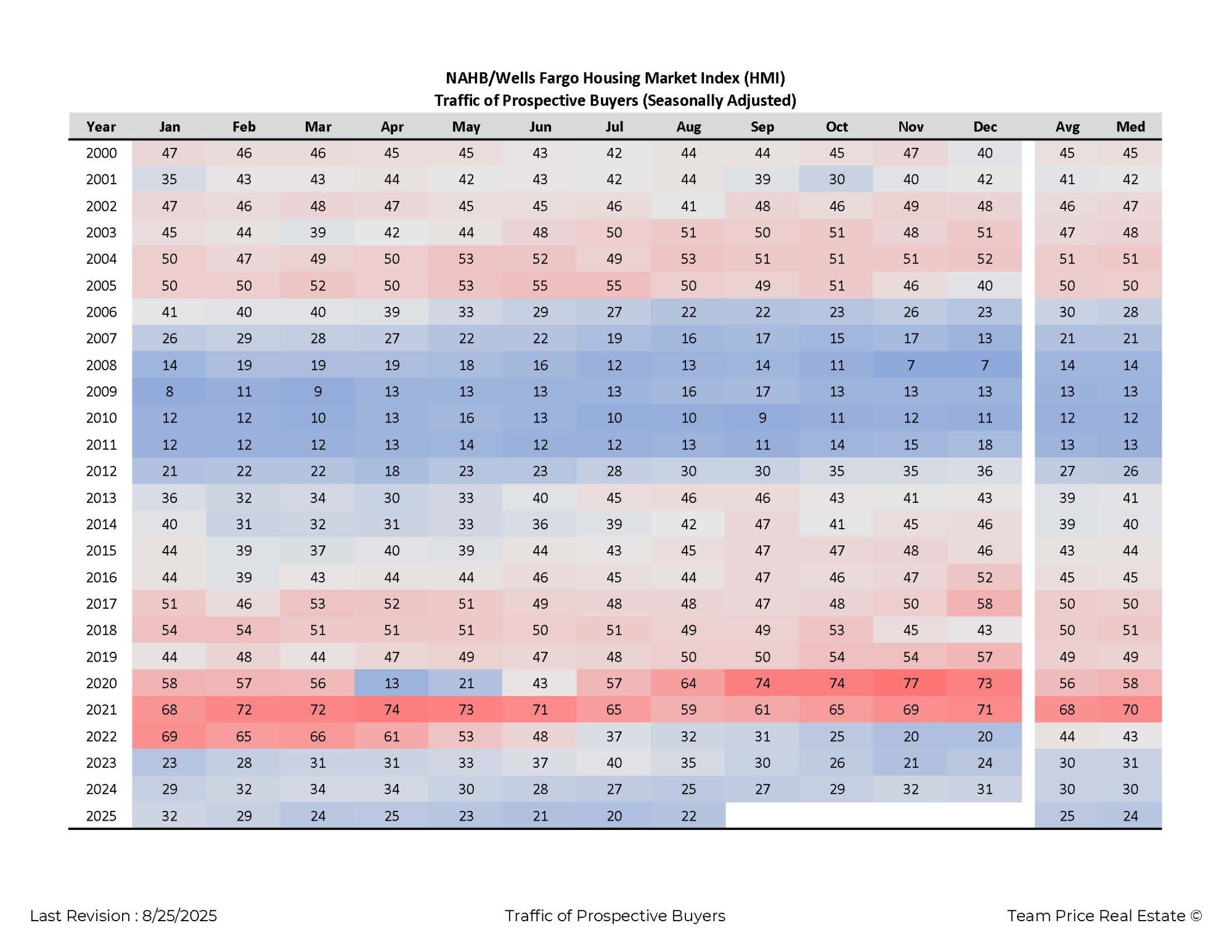

The HMI traffic index, which measures the number of potential buyers visiting new-home communities, shows sharp cyclical changes. After a collapse in spring 2020 due to the pandemic shutdowns, traffic surged to record levels later that year, with monthly readings climbing into the mid-70s. Momentum carried into 2021, when the index averaged near 70, reflecting extraordinary demand fueled by historically low interest rates. That strength reversed in 2022 as rising mortgage rates cut affordability. Traffic dropped steadily, ending the year with readings near 20, a dramatic decline from the peak just one year earlier. In 2023, traffic remained weak, averaging around 30, and by 2024 levels stabilized in the high 20s to low 30s. In 2025, year-to-date figures continue to trend lower, with readings between 20 and 32 through October, underscoring that on-the-ground buyer activity remains well below the highs of the pandemic housing boom.

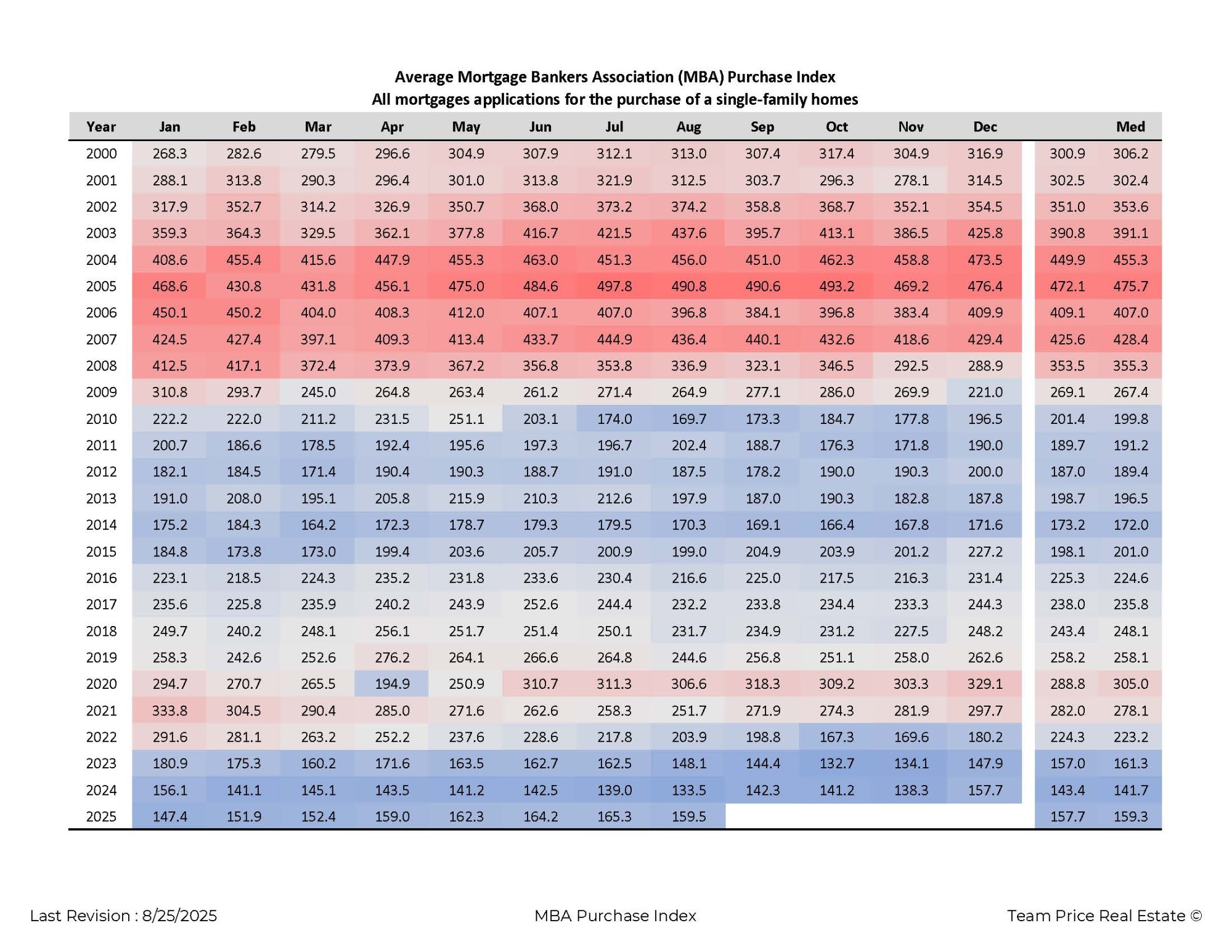

The MBA Purchase Index, which tracks mortgage applications for home purchases, provides another view of demand. Like the HMI, this index spiked in 2020, rising above 300, before easing as affordability tightened. In 2021, the index averaged around 278, down slightly but still strong. By 2022, higher borrowing costs drove the index lower, with monthly averages falling into the low 200s by year-end. The decline continued through 2023, when the index sank below 150 by autumn, reaching its weakest point since the housing recovery of the early 2010s. In 2024, applications stabilized at depressed levels, with monthly figures averaging in the low 140s. In contrast, the first ten months of 2025 show modest improvement, with values ranging from 147 to 165 and averaging near 159. This represents a nearly 10 percent increase compared with 2024, suggesting that buyers are gradually re-entering the market despite ongoing challenges.

Taken together, these data sets highlight a market still in transition. Builder-reported traffic remains subdued, signaling that affordability concerns and cautious consumer behavior continue to weigh on new-home demand. At the same time, the rise in mortgage purchase applications indicates that serious buyers are slowly increasing their activity, likely supported by stabilization in mortgage rates and selective builder incentives. The divergence between traffic and applications suggests that while casual interest has not returned to pre-2022 levels, committed buyers are finding ways to move forward.

As the remainder of 2025 unfolds, monitoring both the NAHB traffic index and the MBA Purchase Index will be critical for gauging whether early signs of stabilization strengthen into a sustained recovery.

FAQ: Housing Market Trends Using NAHB and MBA Data

1. What does the NAHB/Wells Fargo Housing Market Index (HMI) measure?

The NAHB HMI “Traffic of Prospective Buyers” tracks the number of people visiting new-home communities. It serves as a real-time gauge of buyer interest. In 2020–2021, traffic surged to record highs, averaging in the 70s, but dropped sharply to near 20 by late 2022 as mortgage rates increased. By 2025, traffic has remained subdued, averaging in the mid-20s through October.

2. What is the MBA Purchase Index and why is it important?

The Mortgage Bankers Association Purchase Index reflects mortgage applications for home purchases. It indicates buyer intent to proceed with a purchase. After hitting highs above 300 in 2020, the index declined through 2023, falling below 150. However, in 2025 the index shows a modest rebound, averaging around 159, about 10% higher than 2024.

3. How do the NAHB and MBA indexes differ in what they measure?

The NAHB index captures prospective buyer activity—people browsing new-home communities. The MBA index tracks mortgage applications, which represent more committed purchase activity. Together, they provide a fuller picture of both early buyer interest and serious purchase decisions.

4. Why are the two indexes showing different trends in 2025?

In 2025, buyer traffic remains low while mortgage applications are slowly increasing. This divergence suggests that casual browsing is limited due to affordability concerns, while serious buyers are moving forward with financing, supported by stabilizing mortgage rates and builder incentives.